Section

This Tax update highlights a clear shift in how tax and duty outcomes are being assessed. Recent rulings and decisions place greater scrutiny on structures, control and documentation, particularly where long-standing practices rely on timing or informal arrangements.

Below is a brief overview of the key developments and what they may mean for you.

Property Development Structures Which Defer Income Recognition Under ATO Scrutiny

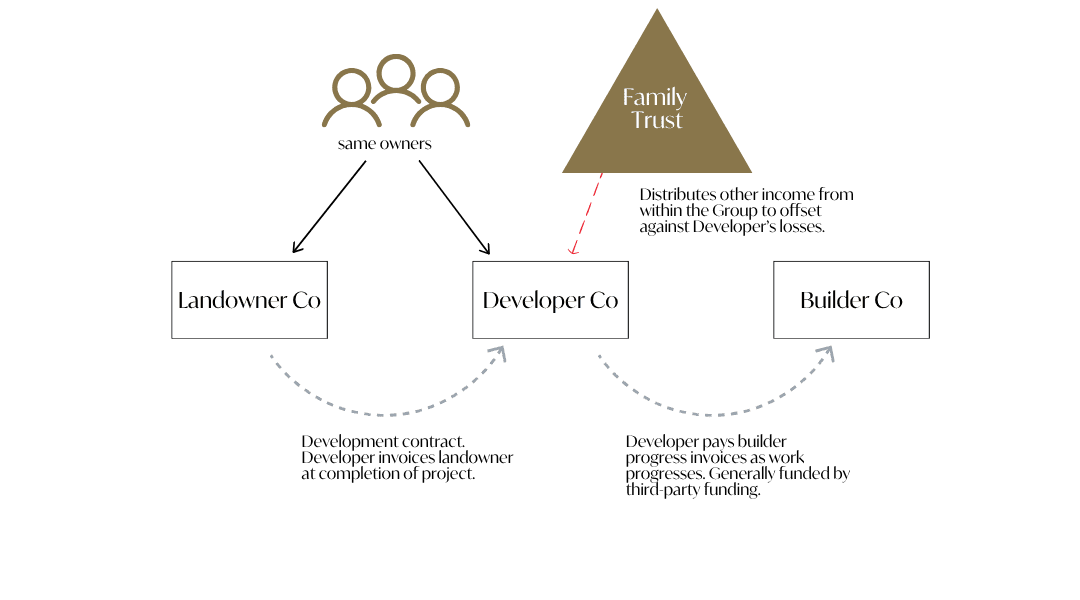

Taxpayer Alerts are issued by the ATO to notify taxpayers of emerging high-risk arrangements which the ATO is actively reviewing. The ATO recently released Taxpayer Alert 2026/1 (“TA 2026/1”) which flags property development arrangements in which a special purpose ‘developer’ entity is established alongside the landholder entity. By separating the development activities from the landholder, the Commissioner is of the view that the Group is able to:

- Inappropriately manipulate the application of the trading stock provisions;

- Defer the recognition of income by the developer entity; and

- Generate losses in the developer entity that are then used to offset income from the broader group.

The key features of these types of arrangements include:

- A special purpose developer entity is interposed in between the landholder and the builder.

- The landholder and the developer entity are under common ownership/control.

- The landholder and the developer entity enter into a long-term development contract under which the developer doesn’t derive any income for managing the development until the project is complete.

- Under the terms of the contract the developer purportedly provides development services to the landowner, but in practice there is minimal or no evidence that the developer does, or has the capacity to, manage the development. That is, the developer exists in form only.

- The services provided to the landowner by the developer are all outsourced to the builder and funded by another party.

- The losses (arising from the deductions claimed progressively for construction costs) are then offset against other income earned by the developer or other income of the Group.

- This arrangement may be repeated in a deliberate manner to coordinate with the timing of income from the broader economic Group or other development projects, resulting in minimal to no tax being paid across the Group.

The following diagram illustrates how these types or arrangements would typically be structured:

The ATO are of the view that these arrangements may fall within the scope of the general anti-avoidance provisions which targets schemes entered into for the dominant purpose of obtaining a tax benefit – and they will actively engage with taxpayers who they believe are involved in such arrangements.

Further, the ATO has advised that they intend to issue a Practical Compliance Guideline (“PCG”) which will outline the ATO’s proposed compliance approach, including indicators of high-risk arrangements and illustrative examples likely to attract ATO attention.

How a Change in Trustee May Trigger Landholder Duty

A recent Victorian Supreme Court decision, Tao v Commissioner of State Revenue, highlighted a potential unknown exposure to duty liabilities by ruling that a change in control of the trustee company of a landholding unit trust alone can trigger a landholder duty liability, even if the underlying beneficial ownership/unit holders remain unchanged.

The Facts: An administrative change with a tax consequence

The case involved a unit trust with a trustee company that owned Victorian land worth more than $1 million, therefore making it a ‘landholder’.

Following concerns about mismanagement, one of the unitholders, Mr. Tao, took control of the trustee company by acquiring all its shares and becoming its sole director. Critically, Mr. Tao did not acquire any more units in the trust itself nor did the land change hands.

However, the Victorian State Revenue Office (“SRO”) viewed this as an “acquisition of control” under Section 82 of the Duties Act. It assessed landholder duty as if Mr. Tao had acquired a 100% interest in the land.

Upon challenging the matter to VCAT, the percentage of the acquisition was reduced to 85% in recognition of the interest Mr. Tao previously held in the land, but the imposition of the duty was upheld.

Mr. Tao appealed the matter to the Supreme Court, however, the court ultimately sided with the SRO and reaffirmed the VCAT decision. It was the first time Section 82 has been challenged, which until now had been seen as merely an anti-avoidance measure.

What this means for you: Key takeaways

This case fundamentally changes the risk profile for unit trusts and private companies that own land.

- Director and Shareholder Changes are Now High-Risk: Appointing a new director, changing shareholders, or any action that results in change of “control” of a corporate trustee of a landholding unit trust or private company can trigger a Section 82 assessment, even for seemingly administrative reasons.

- Common Scenarios may now be Caught: This ruling has ramifications for common business and family arrangements where property is held in private companies or unit trusts, including:

- Succession and Estate Planning: Transferring control to the next generation early by changing the directors of a company.

- Shareholder/Partner Disputes: where a “partner” ceases being a director or shareholder of the trustee company or private company.

- Divorce or Relationship Breakdowns: One party taking sole control of a corporate trustee as part of a settlement.

Given this change, we recommend determining landholder duty exposure before making control changes. Duty implications must now also be considered before making any changes to the board or directors of a corporate trustee or private company, and not simply when buying or selling property.

The risk arises where there has been a substantial change in control of the private landholding entity. The Tao decision has essentially resurrected a previously dormant application of the Duty provisions, potentially exposing all property owners using unit trust or corporate structures.

While the provision is not directly aimed at discretionary trusts, any changes to the control of a corporate trustee of a discretionary trust may still have potential duty implications under this new interpretation of the landholder duty provision and should be reviewed carefully.

The $19 Million Lesson – Why Substantiation Matters

Running a business, particularly within a family or closely-held group, often involves a degree of informality when it comes to inter-entity arrangements. However, a recent decision from the Full Federal Court in Commissioner of Taxation v S.N.A Group Pty Ltd has delivered a warning about the dangers of relying on informal arrangements.

The Court disallowed c. $19 million in tax deductions claimed for service fees paid between related entities for the use of group assets and staff, after their formal written agreement had expired. The businesses could not provide enough objective evidence to prove a new contract existed and that a legal obligation existed in relation to the relevant expenditure.

This decision highlights a critical risk for all business owners that without clear, contemporaneous proof of a legal obligation, even legitimate business expenses could be denied.

The Golden Rule: You Must ‘Incur’ an Expense to Deduct It

This case hinged on the primary general deduction provision contained in section 8-1 of the Tax Act. To claim a general deduction, you must be able to prove that you have “incurred” the expenditure i.e. have an obligation to make the payment. In the case of related party arrangements, that often (but not always) relies on the existence of a formal agreement.

While the Federal Court ruled in favour of the taxpayer, the Full Federal Court unanimously overturned this decision. The Full Court’s reasoning was not about whether the fees were commercially fair, but whether the obligation to pay them was legally enforceable. Not only was there no written agreement in place, but there was no clear communication in relation to the services, the fees were calculated retrospectively, and the payments were intermingled with other inter-entity transactions.

Without objective, contemporaneous evidence to the contrary, the taxpayer failed to meet its legal burden of proving the payments were made under a specific, enforceable obligation and for a commercially justifiable objective. As a result, the outgoings were not “incurred” for tax purposes and the deductions were disallowed.

An Action Plan Before 30 June

This case is a reminder that informality can be costly, as informality does not relieve taxpayers from the statutory onus of proof.

With 30 June approaching, you should:

- Ensure all related-party dealings are properly documented to avoid any ambiguity around the obligations.

- Conduct a review of all arrangements like service fees, loans, and shared asset use.

- Ensure written agreements are current and accurately reflect commercial reality, and update them if required.

Where no formal agreement exists, you should at least ensure the arrangement is properly documented and the legal obligation can be substantiated in order to safeguard your deductions.

If you require assistance with understanding whether your related party transactions are appropriately documented, please reach out to your SIP advisor.

On the Horizon – Are Changes to the CGT Discount Coming?

A Senate Committee report on the operation of the Capital Gains Tax (“CGT”) discount was tabled on 17 March 2026. The committee examined the economic and social impact of the long-standing tax concession.

Key findings of the Inquiry

After a period of public hearings and submissions, the Senate Committee’s report highlighted several concerns with the operation of the CGT discount.

- Distortion of Economic Decisions: The report found that the current design for the concessional treatment of capital gains compared to labour income distorts economic decision-making and creates powerful incentives for tax planning.

- Misallocation of Investment: The committee heard evidence suggesting the discount has the potential to distort the allocation of investment across the economy. A substantial share of the capital gains receiving the discount comes from investments in existing housing stock, rather than more productive areas of the economy.

- Impact on the Housing Market: A key finding was that the CGT discount, particularly when combined with negative gearing, has likely skewed housing ownership away from owner-occupiers and towards investors, contributing to housing affordability pressures.

Potential Reform Options Outlined in the Report

Based on its findings, the report canvassed several policy options for the government’s consideration:.

- Altering the CGT Discount and Calculation Method: Several options considered changing the discount itself. This included simply reducing the 50% discount to a lower figure (ranging from 40% to as low as 10%). More fundamental changes were also explored, such as abolishing the discount entirely or, alternatively, returning to the previous system of indexation.

- Targeted Reforms for Housing and Negative Gearing: The report considered options to treat CGT differently for residential housing investments. This could involve a lower discount for investment in existing housing stock as opposed to new dwellings. It was noted that any meaningful reform to the CGT discount to address housing affordability would likely need to be coupled with reforms to negative gearing arrangements.

- Implementation and Broader Context: The report stressed the importance of carefully managing any transition. A key consideration was whether to “grandfather” existing arrangements. This would mean any changes would only apply to assets purchased after a specific date, protecting current investors from retrospective changes.

What Does This Mean for Investors?

It is important to reiterate that this report does not change any laws. The CGT discount remains in place, and the current rules for eligibility and calculation continue to apply.

However, given the scope of the inquiry, the report’s findings and comprehensive reform options place the CGT discount firmly on the agenda for potential future reform. It’s possible that the Government announces changes to the CGT discount in the upcoming Federal Budget in May.

Guess who’s back, back again – FBT’s back

The 2026 Fringe Benefits Tax (“FBT”) year ends on 31 March, meaning it’s now time to review the benefits provided over the year to employees and their associates to ensure all obligations are met and to manage any FBT liability effectively.

A proactive review before the year ends can prevent unexpected tax bills and penalties.

Your FBT Year-End Housekeeping Checklist

Ahead of the FBT year-end, we have flagged the following points for your consideration:

- Finalise Vehicle Records: Capture the closing odometer readings for all company vehicles and ensure you have the details of any new vehicles purchased during the year. Ensure any employee logbooks are current, and you have collated records of employee contributions towards vehicle running costs.

- Gather Employee Declarations: Collect all necessary written declarations from employees regarding the business use percentage of benefits provided, such as for mobile phones or ‘workhorse vehicles’ taken home by employees.

- Review Entertainment Costs: If you use the ‘actual method’ for meal entertainment, ensure you have detailed records, including the number of employees versus non-employees (e.g., clients) who attended functions/events.

You should always consider whether you have provided any benefits during the year that can trigger a requirement to register for FBT, even if you have not lodged FBT returns in the past.

The Electric Vehicle Exemption

The most significant change impacting the 2026 FBT year is the removal of the electric vehicle (“EV”) FBT exemption for Plug-in Hybrid Electric Vehicles (“PHEV”).

Effective from 1 April 2025, the FBT exemption for ‘zero or low emissions vehicles’ is now limited to:

- Battery electric vehicles.

- Hydrogen fuel cell electric vehicles.

PHEVs acquired on or after this date will no longer qualify for the exemption. An exception exists for pre-existing PHEV arrangements where a PHEV qualified for the exemption before 1 April 2025, and a financially binding commitment was in place (e.g. a novated lease) before this date to continue providing that same vehicle and on the same terms.

Further, although full EVs may be exempt from FBT, they are still considered a Reportable Fringe Benefits which must be included on the respective employee’s payment summary, therefore a calculation of the notional taxable value of the benefit is still required.

Lodgment and Administrative Reminders

- FBT returns are due by 25 June 2026 if lodged by us as your tax agent, or 21 May 2026 if you prepare your own FBT return.

- If your business is registered for FBT but has no liability for the 2026 year, we strongly advise still lodging a ‘Nil’ FBT return.

* * * * * * * *

The above tax summary is intended to be general in nature and does not constitute advice. Should you believe that any of the above matters may be relevant to you or your Group’s particular circumstances, please discuss the specific details with your Slomoi Immerman Partners advisor.