Section

Changes to Queensland Land Tax – No Longer Going Ahead

The Queensland Government proposed to introduce significant changes to the imposition of land tax in Queensland with effect from 30 June 2023. The Queensland Government has done a backflip and announced on 30 September 2022 that they would not proceed with the changes given the strong negative feedback they received from investors and property industry representations.

Out of interest, land tax in Queensland was going to be calculated having regard to the total value of Australian land. This figure was then to be adjusted for the Queensland portion of total land. For a person or entity owning a Queensland property and an interstate property this would have resulted in an increase in their Queensland land tax bill.

FBT Exemption for Electric Vehicles

Significant changes have recently been introduced to how electric vehicles are treated for Fringe Benefits Tax (“FBTâ€) purposes. The provision of certain electric vehicles by employers to their employees will now be exempt from FBT. This change could potentially save $1,000’s in FBT that would otherwise be payable on a standard petrol vehicle.

Key points:

Employers providing employees with zero or low emissions vehicles will be exempt from paying FBT from 1 July 2022 where the following conditions are met:

• The car must be owned or leased by the employer, eg. novated leases.

• The exemption will only be available to cars that are:

– Battery electric vehicles

– Hydrogen fuel cell electric vehicles

– Plug-in hybrid electric vehicles

• The value of the car at first retail sale must be below the luxury car tax threshold for fuel efficient cars ($84,916 GST inclusive for the 2023 income year).

• The car must be first held and used on or after 1 July 2022.

Whilst this an exciting development, there are several aspects to note:

• The provision of any ancillary benefits, such as the installation of EV charging stations, are not covered.

• There is no agreed methodology for calculating the amount of electricity used to charge electric vehicles.

• Although the provision of an EV will be exempt from FBT, they must still be included when determining the employees’ reportable fringe benefits amount.

Small business to receive 120% deductions for certain training and digital adoption expenditure

SMEs are set to receive a bonus 20% tax deduction for expenditure on eligible external training for employees, as well as expenditure that supports digital adoption. The purpose of these tax boosts is to encourage SMEs to foster a more skilled and productive workforce.

The initiatives were first announced in the March 2022 budget of the previous government, with the new Labor government announcing that it intends to introduce it into law, ie. these changes are not yet law.

To qualify, businesses must have less than $50M in annual aggregated turnover. If the additional conditions below are met, businesses will be able to claim a deduction for 120% of the cost of the eligible expenditure.

For example, a business incurring $100,000 on eligible items will be entitled to a tax deduction worth $120,000. The additional $20,000 tax deduction is equivalent to a $5,000 tax saving for a company at the 25% corporate tax rate.

External Training Expenditure

The following is required in order for expenditure on external training to be eligible:

• Expenditure must be incurred on external training for employees.

• The training must be provided by a registered training provider.

• The registered training provider must not be an associated entity of the entity claiming the deduction.

• The expenditure would, in any event, be deductible.

The external training expenditure must be incurred between 29 March 2022 and 30 June 2024. There is no cap on the amount of the bonus deduction that can be claimed on eligible training expenditure (whereas expenditure on digital adoption is capped at $100,000 per year).

Note that this tax boost excludes training of non-employee business owners such as sole traders, partners in a partnership and independent contractors.

Digital Adoption Expenditure

Expenditure must have a direct link to the business’s digital operations. Eligible expenditure may include (but not limited to):

• Digital enabling items, such as hardware (eg. laptops), software (eg. cloud data storage service), and services related to the use of computer networks.

• Digital media and marketing.

• E-commerce.

The digital adoption expenditure must be incurred between 29 March 2022 and 30 June 2023. The bonus deduction can be claimed on eligible digital expenditure of up to $100,000 per year. In other words, the maximum bonus deduction is capped at $20,000 per year.

Changes to sub-trust arrangements/UPES for the purpose of Div 7A

The ATO has finalised its ruling on Division 7A and sub-trusts. Division 7A deals with the management of shareholder loans for tax purposes. This ruling reverses the ATO’s previous position on Unpaid Present Entitlements (“UPEâ€) owing to corporate beneficiaries, such that they will need to be carefully managed to avoid the triggering of deemed dividends within the Group.

Tax Determination 2022/11 (“TDâ€) deals with trust distributions made to corporate beneficiaries that are not paid, ie. UPEs. Trust distributions are commonly made to corporate beneficiaries in order to cap the tax rate on the distributions at the corporate tax rate. However, where the distribution remains unpaid, this will constitute the provision of financial accommodation by the corporate beneficiary back to the trust.

For Division 7A purposes (Shareholder loan rules), the provision of financial accommodation constitutes a loan. As such, the trust will now need to either pay out the UPE or enter into a 7 year principal and interest loan agreement with the corporate beneficiary, to avoid triggering a deemed dividend.

This TD represents a change in approach by the ATO as compared to its previous position dating back to 2010. In its previous stance, the ATO accepted that the UPEs owing to the corporate beneficiaries could be held on sub-trust, ie. the trust could retain benefit of the funds, provided broadly that a 7 or 10 year interest only loan was entered into (with repayment of the principal at the end of the term). In such a situation, the ATO accepted that no financial accommodation had been provided by the corporate beneficiary.

In this TD, the ATO has reversed its stance, such that even if the trust pays interest on the funds retained in the trust (ie. the UPE), financial accommodation has still been provided.

This means that sub-trust arrangements on 7-year and 10-year interest free loans are no longer acceptable. However, existing arrangements of this kind are allowed to see out the loan term under transitional procedures. Upon maturity of the existing arrangement, the loan on sub-trust must then be paid back or converted to a complying Division 7A loan.

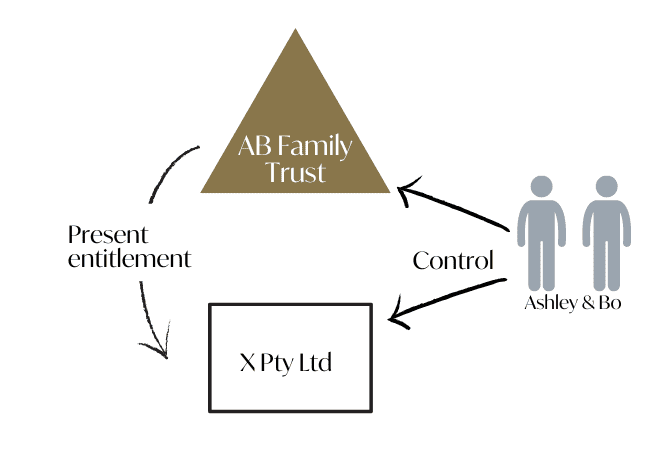

Worked Example – Based on Example 5 in the TD

• Ashley and Bo are spouses and operate their family business via a discretionary trust, AB Family Trust. Ashley and Bo control Trustee Pty Ltd, the trustee of their discretionary trust.

• X Pty Ltd, a private company is a corporate beneficiary of AB Family Trust, and is controlled by Ashley and Bo.

• On 30 June 2023, the Trustee resolves that 100% of AB Family Trust’s income for the 2022-23 income year will be distributed to X Pty Ltd.

• At 30 June 2023, X Pty Ltd does not know the amount of trust income, if any, that it can demand immediate payment of from Trustee Pty Ltd.

• On 1 August 2023, Trustee Pty Ltd determines the net income of AB Family Trust as $50,000. If X Pty Ltd does not demand immediate payment of its entitlement, then it provides financial accommodation to the AB Family Trust in the 2023-24 income year

• The lodgement date of X Pty Ltd’s tax return for the 2023-24 income year is 15 May 2025.

Timeline of events to avoid Division 7A Tax consequences:

From 1 July 2022, a private company beneficiary’s UPE that is held on sub-trust will generally constitute the provision of financial accommodation and trigger Division 7A. This new guidance has been set out in TD 2022/11.

Upcoming Federal Budget – 25th October.

Our next tax update will cover the Federal Budget. The Government has already flagged that the Budget will contain measures to raise extra tax from multinationals operating in Australia. This is unlikely to be a generous Budget as the Government seeks to claw back some large deficits accrued during Covid.