Section

Section 100A: Updated ATO Guidance on Trust Entitlements

Section 100A (“s100A”) of the 1936 Tax Act governs trust distribution arrangements where broadly, the person or entity that actually receives the benefit of a trust entitlement is different to the beneficiary who was entitled to the income.

After issuing draft guidance 10 months ago, the ATO has followed up with its finalised Tax Ruling (TR 2022/4) and Practical Compliance Guideline (PCG 2022/2) explaining the application and compliance approach to s100A.

The ATO’s messaging in the finalised versions has remained relatively consistent with the draft released in February this year. A typical example that the ATO applies is where a distribution is made to an adult child (ie. someone typically aged between 18-22). The distribution is ‘made’ to the child to take advantage of their lower marginal tax rate. However, the actual funds are never provided to the child and typically, the controllers of the trust (eg. the parents) benefit from those funds.

For s100A to apply, a beneficiary must have a present entitlement to a trust distribution (ie. the trustee has resolved to make a distribution to them), and:

- The benefit of the distribution is received by a person other than the beneficiary;

- There is a purpose of reducing the tax liability of one of the parties to the agreement; and

- The agreement was not entered into in the course of ordinary family or commercial dealings.

If the ATO determines that s100A applies, the beneficiary will be deemed to no longer be entitled to the income for tax purposes, meaning that the trustee will be taxed at the top marginal tax rate of 47% on the amount subject to s100A.

The main area of contention, and what will impact most of our clients, is what constitutes ‘ordinary family or commercial dealings’. Despite the ruling being finalised, this aspect is still unclear.

According to the guidance, the core test is whether the dealings can be explained by the commercial or family objectives achieved. The facts and circumstances of each case must be considered, and subjective inquiry is required into what the objectives of the dealings are.

Generally, the mere fact that the arrangement is common, or that all parties to the arrangement are family members, will not, on its own, have the quality of achieving commercial or family objectives. Additionally, the payment of less tax to maximise group wealth is not considered an ordinary family or commercial dealing.

The finalised guidance also discusses the relevance of cultural factors when determining whether a dealing achieves family or commercial objectives.

Where a distribution is not immediately paid to a beneficiary, the ATO’s expectation is that the beneficiary’s entitlement will be paid out within 2 years. Distributions paid out within 2 years of the entitlement arising should remain in the ‘green zone’ (explained further below) and not attract attention from the ATO.

However, it may be the case where an adult child doesn’t call for payment of their trust entitlement until well after 2 years, where for instance, they plan to use the funds for a house or other significant investment. Provided the beneficiary has notified the trustee of their intention to not call for immediate payment, the beneficiary is aware that they can legally call for payment at any time they choose, and the trustee does not apply such funds in an inconsistent way (eg. making a long-term loan to another person), the arrangement should still remain in the green zone.

The PCG now sets out 3 different risk zones so taxpayers and their advisors can assess how the ATO are likely to treat the arrangement.

The 3 risk zones are:

- White zone – applies to arrangements entered into before 1 July 2014. No compliance action will be taken unless already under audit or other scrutiny, or arrangements continue beyond 1 July 2014.

- Green zone – no compliance action will be taken.

- Red zone – will attract the attention of the ATO to conduct further analysis of the arrangement and may lead to audit activity.

Worked Example – Based on Example 7 in PCG 2022/2 – Green Zone

- Homewares Trust is a discretionary trust and carries on a retail business selling homewares.

- The director and shareholder of the corporate trustee is Ms Retail.

- The beneficiaries of Homewares Trust include Ms Retail, her spouse Mr Retail and members of their extended family.

- On 30 June 2023, the trust distributes 50% of the trust income to Ms Retail and the remaining 50% to Mr Retail.

- Mr Retail and Ms Retail use some of their trust entitlements for the 2023 income year to meet their personal expenses during the 2024 income year. The balance of their entitlements remain unpaid and are used to supplement the working capital of the business carried on by Homewares Trust.

- Ms Retail and Mr Retail expect to be paid the remainder of their entitlements but they allow the trustee to use those funds in the homewares business for working capital purposes.

- Funds representing Ms Retail and Mr Retail’s trust entitlements have been either paid to them or retained by the trustee for working capital of the business. The unpaid present entitlements are used to achieve commercial objectives.

- This is an example of an arrangement falling within the green zone and would therefore be accepted by the ATO without further review.

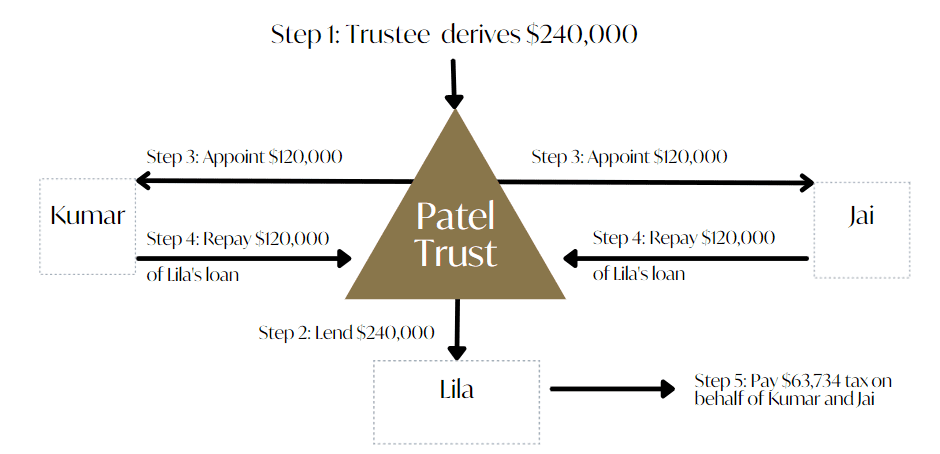

Worked Example – Based on Example 14 in PCG 2022/2 – Red Zone

- Patel Trust’s beneficiaries include the members of the Patel Family. Patel Co is the trustee of Patel Trust, and Lila Patel is the sole shareholder and director of the trustee.

- Lila is the parent of three adult children who all live at home – Sima (aged 26), Kumar (aged 21) and Jai (aged 19).

- During the 2022-23 income year, Sima is self-employed and has a taxable income of $90,000. Kumar and Jai study full-time and derive no income during the income year.

- During the 2022-23 income year, Patel Trust derives $240,000 in income. Throughout the year, Patel Co (the trustee) makes regular payments totalling $240,000 into Lila’s bank account to meet her personal living and household expenses. Those payments are recorded as a ‘beneficiary loan’ in the accounts of Patel Trust.

- On 30 June 2023, Patel Co resolves to make Kumar and Jai each presently entitled to $120,000 of the Patel Trust income.

- Patel Co records these entitlements as being fully paid by applying them against the beneficiary loan owed by Lila. Lila assists in the preparation of Kumar and Jai’s tax returns and pays the tax liability arising in relation to their entitlements from her personal funds.

- The entitlements of Kumar and Jai are applied in this manner because they each purportedly have an outstanding debt owed to Lila in respect of education expenses and their share of the Patel household expenses that Lila paid before they each turned 18.

- The PCG specifically states that an arrangement will fall within the red zone where an adult beneficiary’s present entitlement is paid to the parent or other caregiver of the beneficiary in connection with expenses incurred by the parent or the caregiver before the beneficiary turned 18 years of age, including where the entitlement is applied against a debit balance in the trust’s accounts (such as a loan).

We will continue to consider the ATO’s finalised guidance and will monitor any further feedback from the ATO and industry to ensure we are in a position to assist clients with their trust distributions for the 2023 income year and future income years.

Significant Changes on the Way for Claiming WFH Deductions

The ATO’s release of PCG 2022/D4 introduces a revised fixed-rate method for calculating the deduction an individual can claim for expenses incurred while working from home. The revised method will replace the previous fixed-rate method and the temporary Covid shortcut of 80c per hour, which came to an end on 1 July 2022. However, the actual cost method is still available if you wish to calculate your actual expenditure incurred while working from home.

Under the old fixed-rate method, taxpayers were entitled to a fixed-rate deduction of 52c per hour for the following running expenses:

- Electricity and gas

- Home office cleaning and repair expenses

- Decline in value of office furniture and furnishings

The revised fixed-rate method provides a fixed-rate deduction of 67c per hour, covering the following expenses:

- Electricity and gas

- Internet expenses

- Mobile/home phone expenses

- Stationery and computer consumables

While the fixed rate has increased from 52c to 67c, it now incorporates some additional expenses. This means that taxpayers will be unable to claim a separate deduction for those items, with the main area of concern being the inclusion of mobile phone and internet expenses. Even if you use your mobile phone for work purposes at home and at the office, the guideline specifically discusses that a separate deduction for the office portion of your mobile expenses will not be allowed.

Conversely, taxpayers can now separately deduct the decline in value of depreciating home office assets (such as an immediate deduction for home office furniture purchased for less than $300). However, we expect that overall, the revised fixed-rate method will disadvantage most taxpayers.

Additionally, the updated guidance includes stricter record keeping requirements to verify hours worked from home.

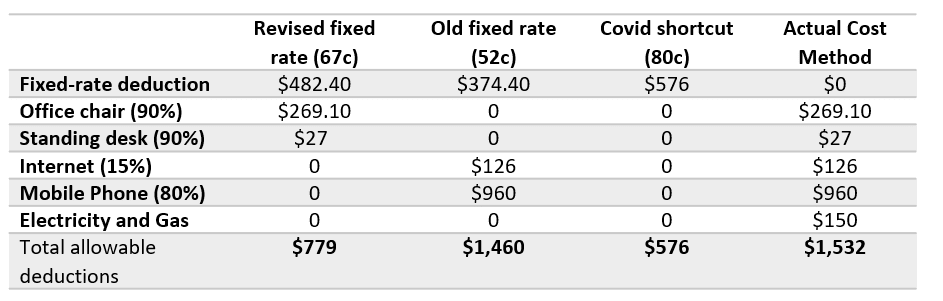

Below is an example demonstrating how the changed methodology impacts allowable deductions relating to working from home expenses.

Example:

During the income year, Cathy kept a diary which shows that she worked 720 hours from home (approximately 2 days a week). Throughout the year she incurred the following expenses:

- Purchased a new office chair for $299 on 1 July – used 90% for work purposes.

- Purchased a standing desk for $600 on 1 July – used 90% for work purposes.

- Home internet bills totalled $840 for the year – Cathy estimates that 15% of her home internet usage is for work purposes.

- Mobile phone bills totalled $1,200 for the year – Because Cathy uses her mobile phone as her work phone on the days she is at home and in the office, she estimates that 80% of her mobile phone expenditure relates to work usage.

- Electricity and gas usage incurred while working from home of $150 (assume this has been calculated using an acceptable method with adequate records).

Based on the items covered by each method, Cathy is allowed to claim the following deductions:

Using the revised fixed-rate method rather than the old fixed-rate method, Cathy’s net allowable deductions have decreased by $681.

Not only will the revised method lead to lower deductions in most cases, but the updated guidance requires quite onerous record-keeping requirements for relatively minor expenses.

With the introduction of the revised method, it may be better in some cases to apply the ‘actual cost method’ to claim relevant expenses, but should be given in ensuring the correct records are maintained.

This new guidance is still in draft and has not yet been finalised, so we will be hoping for added clarity when the final version is released and a relaxation of some of the record keeping requirements.

Changes to Off-Market Share Buy-Backs

As discussed in our Federal Budget insights in October, the Government announced changes to the treatment of off-market share buy-backs. The change means that where a listed public company initiates an off-market buy-back of shares, no part of the amount paid to shareholders will be taken to be a dividend. The whole amount will be considered as a capital payment, as is the case with on-market buy-backs (an on-market buy-back being where the company buys its own shares on the stock exchange in the ordinary course of trading).

This measure will stop a tax-effective return of funds from public companies through “streaming” franked dividends to shareholders. This will predominantly impact self-managed super funds and low-income retirees – those who would otherwise benefit from a refund of franking credits.

Additionally, distributions by listed companies that are considered consideration for the cancellation of a membership interest as part of a selective reduction of capital will also be unfrankable.

The amendments made by the Bill will apply to buy-backs and selective share cancellations undertaken by listed companies that are first announced to the market after Budget night, ie. from 7:30pm on 25 October 2022.

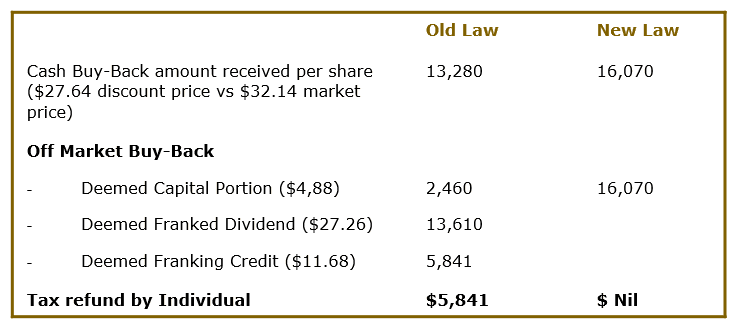

Below is an example based on the BHP off-market share buy-back from December 2018 (based on 500 shares) for a low-income retiree:

From the above scenario, the low-income retiree would be worse off by $3,591 (ie. the refund of $5,841 of franking credits is no longer available, but the shareholder would be paid the market value of $16,070 instead of the discounted amount of $13,820 for their 500 shares).

Budget Recap and Updates

FBT Exemption for Electric Vehicles

The long-awaited Fringe Benefits Tax (“FBT”) exemption for fuel-efficient vehicles has now been legislated. Under this initiative, fuel efficient vehicles are exempt from FBT, subject to the following conditions:

- The vehicle must be either a battery electric vehicle, a hydrogen fuel cell electric vehicle or a plug-in hybrid electric vehicle.

- The vehicle must be first held by the employer (owned or leased) on or after 1 July 2022.

- In the case of second-hand vehicles, the first retail sale of the vehicle must have occurred after 1 July 2022.

- The vehicle must meet the definition of a ‘car’ for FBT purposes (ie. less than 1 tonne carrying capacity and designed to carry less than 9 people).

- The purchase price of the car must be below the luxury car tax threshold ($84,916 GST inclusive for the 2023 income year).

There are several additional factors which should be considered before utilising this concession, which we are happy to discuss with you further.

Super Downsizer Contributions

- The Super Downsizer scheme allows for a one-time contribution of up to $300,000 of the proceeds from the sale of your main residence into super where you have owned the house for more than 10 years and you meet the eligibility criteria.

- As part of the October Budget, the government announced that individuals aged 55 and over (down from 60) will now qualify if the contribution is made on or after 1 January 2023. This proposed change is now law.

- Super Downsizer contributions do not count towards your non-concessional cap (“NCC”) and are not impacted by your total super balance (ie. regardless of whether the balance is greater than $1.7M at 30 June 2022). It does, however, impact eligibility for the Age Pension.

- You don’t actually need to downsize your house or even purchase another house, as long as you meet the eligibility criteria.

- While the Downsizer contribution does not count towards your NCC, it will impact the availability of future non-concessional contributions as it will increase your superannuation balance. Therefore, discussions around timing of contributions are advised.

* * * * * * * *

The above tax summary is intended to be general in nature. Should you believe that any of the above matters may be relevant to you or your Group’s particular circumstances, please discuss the specific details with your Slomoi Immerman Partners advisor.